Getting A Better Read On The Value Of Smartphone Paid Search

The increasing ubiquity of mobile devices has been a mixed blessing for paid search advertisers. On the one hand, most industry stats show smartphones and tablets driving nearly all Internet traffic growth, while volume from traditional desktop and laptop computers has begun to fade. But as more consumers have taken to using new devices for […]

The increasing ubiquity of mobile devices has been a mixed blessing for paid search advertisers. On the one hand, most industry stats show smartphones and tablets driving nearly all Internet traffic growth, while volume from traditional desktop and laptop computers has begun to fade.

But as more consumers have taken to using new devices for browsing the Web, their propensity to buy products or otherwise convert still appears much weaker on smartphones than it does on computers or tablets. This has left many advertisers facing a marketplace where their fastest growing audience is often their worst performing by traditional measures.

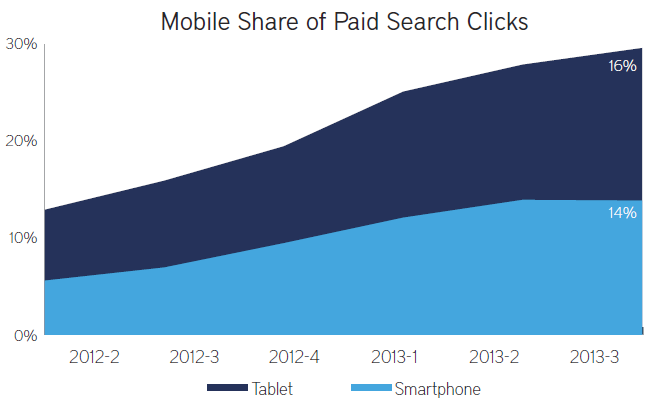

Source: RKG Q3 Digital Marketing Report

This apparent performance gap has persisted over the last few years of rapid smartphone growth, leaving advertisers to face the enduring question of whether smartphone clicks are more valuable than they appear or whether user behavior on different devices is really that disparate.

Google’s Cross-Device Conversion Estimates

While advertisers have done their best to understand the full value of their online traffic, we are forced to work with a limited data set when it comes to more complicated conversion paths. It’s easy to conjecture scenarios where our customers find us on one device and convert on another, but actually tying those two activities together requires the type of connective information that most individual advertisers won’t have for very many users.

By comparison, Google has a wealth of knowledge about individual users, regardless of which device they are on. Through its various platforms and products like Android, Gmail, Google+ and Chrome, Google gets hundreds of millions of users to log into Google accounts routinely. This October, Google revealed that it had 300 million monthly active “in stream” Google+ users. In 2012, Google announced that Gmail alone had 425 million monthly active users worldwide.

While that certainly doesn’t cover every man, woman or child, it is still a huge data set that Google can use to extrapolate some pretty accurate figures on overall cross-device behavior and conversions.

In October, Google officially announced they would be providing advertisers with some of these insights via the new Estimated Total Conversions metric in AdWords, which features cross-device conversions initially with plans to include phone calls and in-store visits in the coming months.

At RKG, we were excited to be early testers of this new feature and we see it as an important step toward marketers achieving greater clarity into the full impact of their ad campaigns. Google clearly has a strong interest in advertisers perceiving ad clicks as being more valuable, but we believe they are being judicious in their calculations and making a long-term play to gain trust in their methodology and figures.

So what does the data tell us so far?

Early Cross-Device Results by Device Type

The original Google announcement noted that cross-device tracking allows travel advertisers to measure 8% more conversions overall, but 33% more conversions for mobile phones. Travel sites may see some of the largest gains for smartphones under cross-device tracking; but, advertisers across nearly all verticals can expect phones to reap bigger conversion increases than computers and tablets.

Looking into the data for our clients, RKG is seeing some variability across sites, but numbers that are generally in line with Google’s initial findings. Cross-device conversions are raising total conversion volume by a range of 2-7%.

For smartphones though, those same sites are seeing a lift in conversions of between 9-33%. The conversion lifts are similar when segmenting by brand and non-brand queries.

Potential Effects On Paid Search Bidding

The cross-device data Google has made available confirms most advertisers’ suspicions that desktop conversions are seeded by smartphone advertisements at higher rates than the reverse. How might this affect the paid search bidding strategy for a typical site?

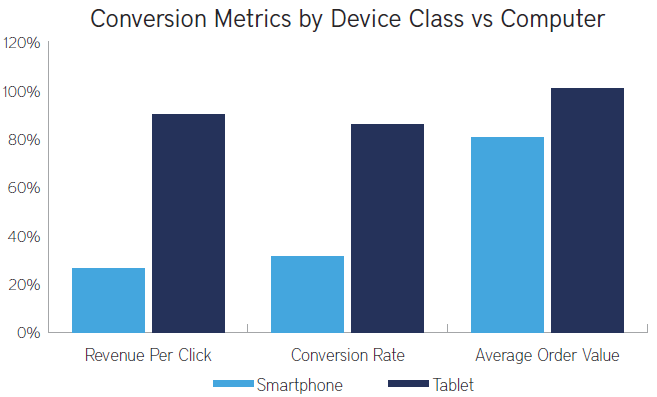

Let’s consider some baseline conversion figures. For the third quarter of 2013, RKG found the average online conversion rate of a smartphone click was just 31% that of a desktop or laptop click. Average order value (AOV) was 20% lower on smartphones, leading to an average smartphone revenue-per-click that was about 25% of desktop levels:

Source: RKG Q3 Digital Marketing Report

A typical retailer might generate an average revenue-per-click of $4.50. For smartphones, that same advertiser would expect to generate a revenue-per-click of about $1.14. If that advertiser had a $5.00 return on ad spend (ROAS) target and bid both desktop and smartphone clicks based only on directly measurable online sales, their desktop cost-per-click (CPC) would average $0.90, while their smartphone CPC would be 25% of that at $0.23.

Adding 33% more orders to smartphones based on cross-device conversions, would drive smartphone CPCs up 33%, assuming no degradation in AOV; but, smartphone CPCs would still be just 34% of desktop levels. Cross-device conversions contribute slightly to the totals for desktops and tablets as well, but not enough to change these figures much.

When we look at how smartphone CPCs have actually been shaping up against computer CPCs, either from RKG or other data sources, it would appear that most advertisers have already been baking in some notions of hidden or indirect value into their smartphone bids. In Q3 2013, RKG found smartphone CPCs running at 38% of desktop levels.

If direct response online conversions were our only concern, whether those conversions occur across devices or not, the numbers suggest that smartphone clicks have already been getting some benefit of the doubt.

Going Offline

For many advertisers, though, online conversions are just one piece of the larger value of search advertising. As Google incorporates additional data into the Estimated Total Conversion metric, like that from in-store visits and phone calls, advertisers will continue to gain perspective on the full impact of their efforts across devices, online and off.

Phone tracking is generally well-established and both RKG and Google have had methods in place for some years now that allow advertisers to directly track or estimate orders from phone calls.

For retailers and other businesses with brick and mortar locations, understanding and quantifying online to offline behavior holds even greater potential to shift advertiser spending strategies. It is a difficult problem, though; and, certain methods of doing so could raise privacy concerns. And, methodology appears to be critical here.

Some sources have estimated that the ratio of online to offline sales generated by online marketing is 1:6 or even 1:10, but RKG studies have shown the ratio is probably closer to 1:0.5. Still, if advertisers can quantify offline spillover more accurately and consistently, even the lower end of that spectrum could produce significant changes in bidding strategies.

As with cross-device tracking, advertisers should welcome Google getting into the offline tracking space; but, we should expect them to apply statistically rigorous methods. Google has a strong incentive to pursue this path, and the scale to do it well; but, they will need to convince advertisers of the veracity of whatever view of this data they ultimately provide.

Lastly, if Google really wants all of their promising data to have a major impact on bidding, they would be wise to ensure that their API capabilities around it are robust and built-out quickly. Enterprise advertisers and sophisticated SMBs view paid search performance through the larger prism of multichannel attribution, which benefits greatly from, and often requires, granularity of data.

Opinions expressed in this article are those of the guest author and not necessarily Search Engine Land. Staff authors are listed here.

Related stories

About the author