The biggest Google ad updates are also the quietest

Advertisers have seen many big updates from Google over the past year, but columnist Andy Taylor makes the case that the most impactful updates may well have been the least publicized.

Expanded text ads. The removal of right-rail ads and the addition of a fourth text ad at the top of desktop searches. Customer Match.

These are just a few of the “major” Google announcements made over the past year that caused big reactions across the search industry. Analysts, myself included, have been scrambling to report on how these updates are impacting brands and to come up with best practices in light of the results.

Analyzing the paid search landscape, however, I find that it’s often the silent, unannounced updates that have the largest impact on performance.

Of course, all paid search managers would love to think that the success or failure of their programs hinges on their hard work and brilliant strategies, but sometimes the most significant factors happen behind the scenes.

That’s not to say that there aren’t smarter ways than others to respond to these unannounced developments, and it can pay to be able to figure out they’re happening in the first place.

To illustrate my point, I’ll discuss a few recent updates that have received a lot of coverage and a few that are less well publicized, then explain how each update stands to impact performance.

Well-known but less impactful updates

Expanded text ads

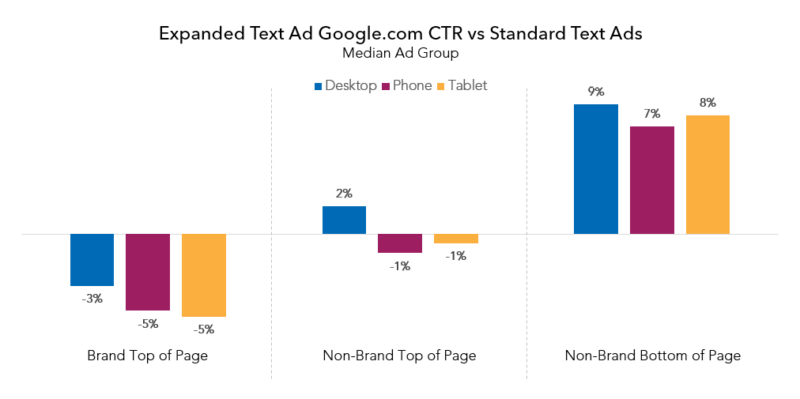

Google’s new expanded text ad (ETA) format offers significantly more characters for advertisers to work with and was touted by Google itself as increasing click-through rate (CTR) by 2X for some advertisers.

I wrote extensively on the early performance comparisons between ETA and older text ads here a month ago, explaining that when the data is segmented properly, non-brand ads at the top of the page see almost no difference in performance. ETAs for brand terms at the top of the page actually had slightly lower CTR than the older ad format.

ETAs at the bottom of the page do appear to be outperforming standard text ads in CTR, but the bottom of the page only accounts for about 20 percent of all non-brand clicks, according to our data at Merkle. This means the overall impact on account performance from a better CTR in this page location is slight.

I explained in my prior post why it’s likely that some case studies that have been published show much better results with ETA, and you should go read that if you’re interested in understanding more about how ETAs are really performing.

To the point of this post, our outlook is that ETAs will likely have a much smaller impact on ad spend than the reactions it has garnered might indicate.

Customer Match

Hailed as the beginning of futuristic search targeting, Customer Match provides advertisers the ability to create audiences out of email lists in order to adjust bidding and messaging for those users when they search.

Using information about users in Customer Match audiences, such as past order history, advertisers would then be able to “personalize” the ad experience in order to drive greater value out of paid search.

Across Merkle advertisers actively deploying Customer Match audiences, only about two percent of Google search spend is being attributed to them, largely due to the limited share of emails Google can match to searchers and the restriction that all emails used in these audiences must be obtained firsthand by each advertiser.

The share of orders is higher (as these users are typically very high-value and more likely than an average searcher to convert), but still small.

There are certainly possibilities on the horizon that could help to increase spend and order share, some of which I’ll be speaking to in an upcoming SMX East session devoted entirely to Customer Match.

However, the current reality and short-term outlook is that while Customer Match does allow for some unique targeting options in crafting catered experiences to users that a brand has interacted with previously, it’s not able to reach a large share of searchers in general.

Tablet bidding controls

Google recently announced that advertisers will be able to set bids for desktop and tablet devices separately, eliminating one of the more annoying aspects of Enhanced Campaigns to date.

I myself was pretty pumped for the update. I can’t deny that.

But digging into what the real impact on ad spend will be, it’s likely pretty small.

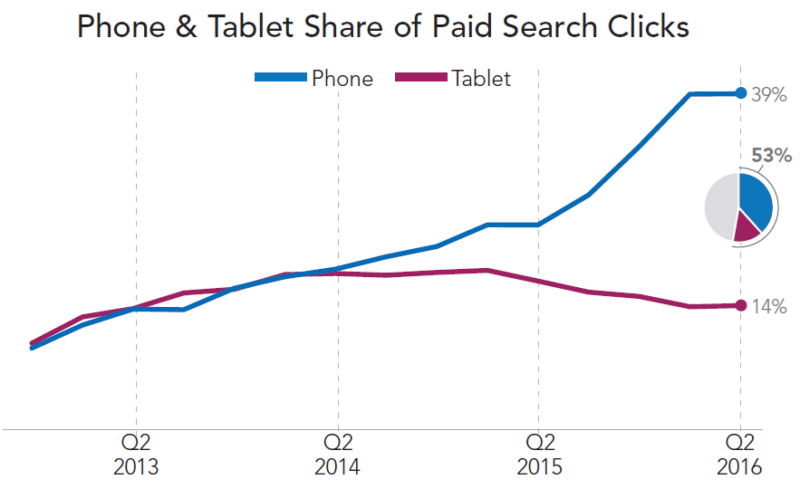

While most advertisers will likely quickly move to bid tablets down relative to desktop due to lower conversion rates on tablets (tablet revenue per click was 30 percent lower than that of desktop for Merkle advertisers in Q2), tablet paid search traffic share is declining.

In fact, it’s been declining for the past several quarters, and was down to 14 percent in Q2 2016, compared to its high point of 18 percent in Q1 of 2015.

Sales numbers verify the waning popularity of tablet devices, and as smartphones get larger and more sophisticated, it is possible tablets continue to shrink as a share of paid search traffic.

At present, decreasing tablet devices in a vacuum by 30 percent in and of itself has the potential to decrease total paid search investment by perhaps four percentage points for our advertisers, with that impact becoming smaller if tablets continue to decline in importance.

However, decreases in tablet bids should accompany increases in desktop bids, as the value of desktop traffic should warrant higher bids than the combined value of desktop and tablet traffic. If all desktop bids increased properly, given the relative revenue per click of desktop versus tablet we observe for our advertisers, this has the potential to result in about a three- to four-percentage point bump in total paid search spend taken in a vacuum.

And assuming that most advertisers will move similarly to take advantage of the new bidding controls, the overall competitive landscape on these devices shouldn’t shift too much.

The overall difference in spend, then, is likely to be pretty small.

There are, of course, industries in which advertisers might see better performance on tablets, such as gaming apps. But again, it’s likely that all of the players in these industries will react similarly to the changes, and the bid adjustments made to desktop and tablet will impact spend on these device types in opposing ways much like for advertisers that see worse performance with tablets.

More than anything, the device split feels like a moral victory for advertisers who have been clamoring for these controls since the beginning of Enhanced Campaigns. Google waited until tablets were on the decline to hand over control, however, and the overall impact could be pretty small.

Important changes that haven’t been well publicized

Google adds third (and fourth) text ad on phones

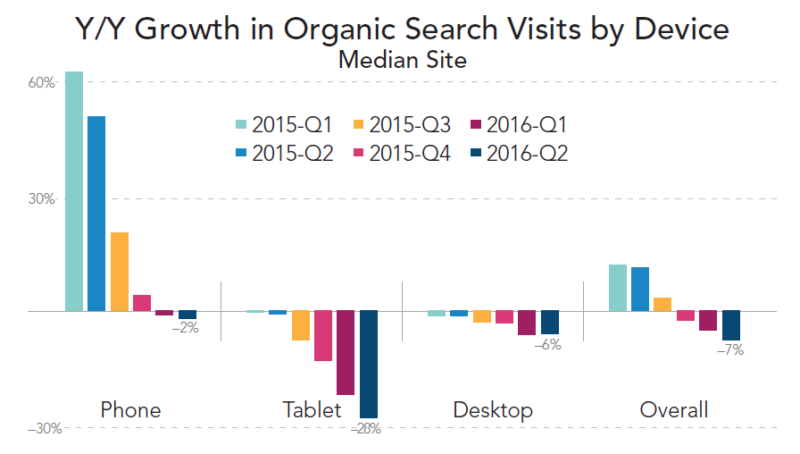

In mid-2015, Google silently released a third text ad above the organic links on phones, formally admitting to the change in late August after a post of mine reported on the impact of the change. The third text ad has been a significant driver of paid search spend growth ever since.

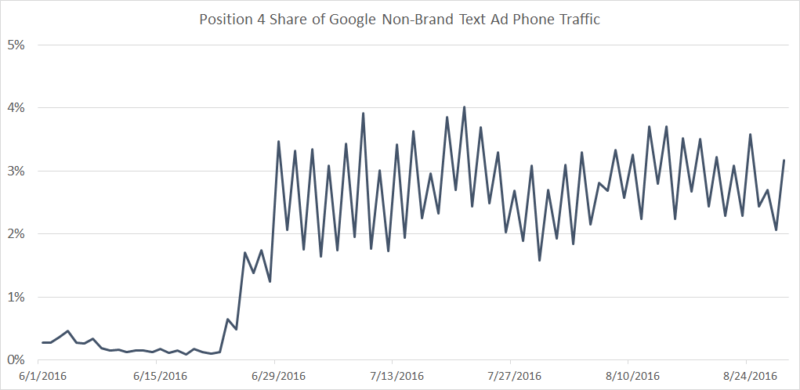

One year after the addition of the third text ad, Google moved to add a fourth text ad to some queries, again with no formal announcement and also no real confirmation.

This has significantly driven up the share of phone traffic coming from the fourth ad position on phones, from close to zero in early June to about three percent now.

The third text ad increased the maximum number of text ads above organic links on phones by 50 percent. The fourth text ad increased it by 33 percent.

As such, it’s no wonder why organic traffic growth on phones has been in decline over the past year.

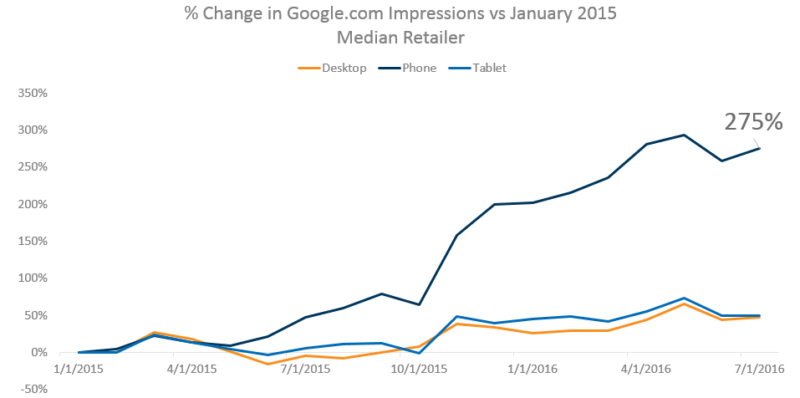

Google rapidly expands Product Listing Ad (PLA) impressions on google.com

The graph below features the change in Google Shopping impressions relative to January 2015 over the past 19 months.

As you can see, Merkle advertisers saw more Google Shopping/PLA impressions in Q1 of 2016 than they did during the busy holiday season of 2015 (by far the busiest season for the vast majority of our advertisers). Looking at a Y/Y comparison, January 2016 saw 202 percent more phone PLA impressions than January 2015.

Further, PLA impressions have continued to increase throughout 2016, particularly on phones.

In turn, PLA spend growth on phones has been rather incredible, with a Y/Y increase of 135 percent in Q2 for Merkle retailers.

No formal announcements explain these trends, and this is just for Google.com.

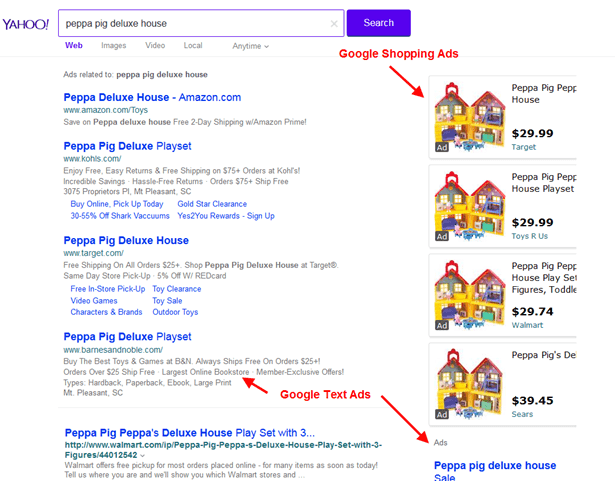

Quiet expansion of the PLA search partner network

PLA search partner traffic share has exploded over the past few quarters, and it now accounts for 14 percent of all desktop PLA traffic.

This rise can be attributed to a few changes.

One is Google’s move in December of last year to begin showing PLAs in Google image search, a move which Google only formally announced six months later.

Another is Yahoo’s apparent shift to increasingly showing Google PLAs in its results, as opposed to Bing Ads or Gemini Product Ads.

The rekindling of the Yahoo–Google relationship was formally announced last October, and Yahoo has spoken of their efforts to choose the best ads from AdWords, Bing Ads and Gemini in recent quarterly earnings calls. Still, the expansion of Google PLAs on Yahoo.com seems to be garnering little attention from many in the SEM industry.

Conclusion

In the case of two-sided businesses like Google that have to serve not only the public but also advertisers, it can be necessary to be very vocal about some updates, while offering no public acknowledgment whatsoever of others.

In most circumstances where they remain mum, I imagine Google’s reasoning usually has to do with there being no obvious positive outcome of a formal announcement.

Judging by how the search industry reacts to the announcements that are publicly made, we tend to jump on Google’s statements with a pretty critical spotlight, so it’s not shocking that they’d want to avoid controversy when possible. Not every decision can make every party happy.

However, Google’s silent updates have been steadily impacting our advertisers’ performance far more than the most publicized changes. This is something to keep in mind when analyzing paid search performance and attempting to explain shifts.

Contributing authors are invited to create content for Search Engine Land and are chosen for their expertise and contribution to the search community. Our contributors work under the oversight of the editorial staff and contributions are checked for quality and relevance to our readers. The opinions they express are their own.

Related stories

New on Search Engine Land

About the author